Inflation looks stubbornly persistent, and the economy is more robust than expected. How much longer can the Fed stick with its current plan of attack?

Two months into 2023, the Federal Reserve is still fighting the battle against post-pandemic era inflation that began in early 2022. Like all wars, this one has multiple fronts and a “fog of war.” The battle capitulates from high inflation to recession and job loss. Conflicting data points and noise created by repercussions across the global economy reeling and rebounding from the pandemic extremes have concealed battlefield conditions.

James B. Bullard, Chief Executive Officer of the Federal Reserve Bank of St. Louis, gave an extended interview on CNBC on February 22, sharing his perspective on the current economic conditions and federal reserve policy. His first point is that the Fed’s first 2 ½ % rate increases only returned the funds rate to pre-pandemic levels. He also discounted the risk of recession, citing readings of low economic stress, and pointed to letting inflation remain at current levels or reaccelerating as the nation’s most significant risk. He punctuated his case for faster rate hikes now, “It is a great time to fight inflation because the labor market is so strong.”

Bullard also set the context of global economies as analogous to the inflation that has historically been experienced post-war. Paraphrasing, the government spends a lot to fight a war with little concern about future tax consequences, and monetary authorities are asked to keep rates low to help the war effort. High fiscal spending and loose monetary policy usually result in undesirably high inflation. Post-war, the government reigns in spending, and monetary authorities tighten financial conditions to battle inflation. A year into Federal Reserve tightening and with a debt ceiling budgetary battle brewing, Bullard’s analogy sums up where our country finds itself today.

Throughout the Fed’s current battle with inflation, the stock market has acted as a barometer for the struggle: as inflation weakened, stocks rallied, and vice versa.

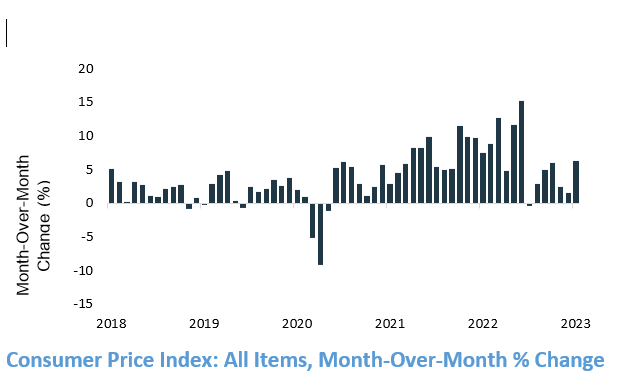

In 2022, the Fed’s attack strategy of raising rates worked well as consumer price inflation eased for three consecutive months. From the market’s low in October to its recent high in early February, the S&P 500 rallied 17%. But new data showing an upturn in inflation and a stronger-than-expected economy have demonstrated that victory is not quite yet at hand.

Source: Kestra Investment Management, U.S. Bureau of Labor Statistics with data from Federal Reserve Bank of St. Louis. Data as of February 28, 2023.

Will Inflation Ever Subside?

While inflation is typically discussed and used as a “catch-all” term for prices, it’s actually comprised of the movements of multiple types of prices throughout the economy. We can break these sections into three broad categories: goods, shelter, and wages. Right now, each category occupies a different stage of the fight against inflation, some better and others worse off.

Goods

Goods prices include a wide variety of tangible items for purchase, including products such as cars, eggs, and gasoline. These types of prices tend to move more dramatically and more quickly than other types of prices. Recently, with help from lower commodity prices, consumer durable goods prices – a subset of consumer goods – are actually lower than they were a year ago, and leading indicators suggest further easing. Supply chains have come unsnarled, pushing the rate to ship a container overseas to pre-covid levels, helping to drive down the end costs of many consumer goods. Meanwhile, various surveys suggest that medium and long-term inflation expectations are back to normal ranges.

Shelter

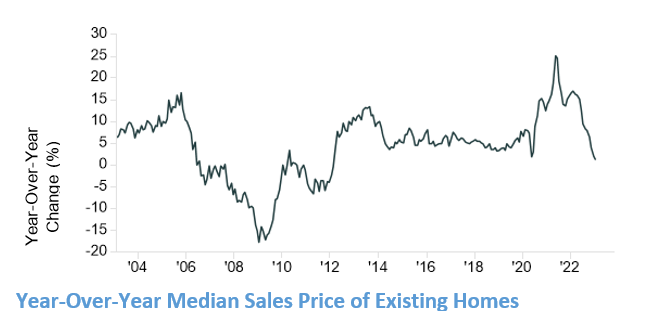

Shelter prices consist of two major components – home prices and rent – which tend to move much more slowly than goods prices. That said, we are seeing signs of easing. As of January, existing U.S. home sales have decreased for twelve consecutive months. That dramatically slower buying activity takes time to filter through to broad measures of housing prices, yet that too is beginning to happen. In January, the median sales price of existing homes increased by just 1.3% to $359,000, the smallest annual gain since February 2012.

Source: Kestra Investment Management, U.S. National Association of Realtors with data from FactSet. Data as of February 28, 2023.

Wages

With both goods and shelter prices easing, what’s all the fuss about inflation? The short answer is wages, which tend to move more slowly and, as such, once elevated, are much more difficult for the Fed to combat. Annual wage growth in the private sector remains high at 6.1% as of January, after peaking last August at 6.7%. Helping drive those wage gains, jobs remain plentiful as employers added an astonishing 517,000 jobs last month. Despite employers increasing wages to try and keep pace with inflation to retain talent, it is estimated that 66% of Millennials and 72% of Gen Z workers are planning to switch jobs in 2023, suggesting that it will be difficult for employers to hold the line on further wage increases.

What Does All This Mean for Investors?

With the Fed and inflation still fighting in the trenches of this prolonged battle over prices, investors should continue to expect more turbulence ahead in 2023. Based on the latest data showing a stronger economy and still-rapid price increases, the Fed will likely raise rates multiple times over the next few months to further slow economic growth. While the prospects of a hard, soft, or no landing remain hotly debated, investors with well-diversified portfolios that stay the course despite market gyrations should be positioned for solid long-term growth.

The first quarter is always a good time to review your financial plan and investment portfolio as we head into tax season. Your February portfolio reports have been deposited into your eMoney vault, and we are contacting clients to schedule reviews. If you want to discuss your plan and portfolio sooner, click here to schedule a convenient time.

Thank you for the trust you place in us. We look forward to connecting soon!

Tim

___________________________________________________________________________________

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation. Comments concerning the past performance are not intended to be forward-looking and should not be viewed as an indication of future results.

Converting a traditional IRA to a Roth IRA is a taxable event and could result in additional impacts to your personal tax situation, including the taxation of current social security benefit payments. Be sure to consult with a qualified tax advisor before making any decisions regarding your IRA.