2022 began with the Federal Reserve pivoting away from an “easy money” policy because they believed inflation was transitory, to rapidly tightening monetary policy at a historic pace having realized inflation had become a problem. That was the economic and market backdrop for the year, Russia invading Ukraine exacerbated uncertainty and inflationary pressures, but tighter monetary policy and the resultant higher rates and uncertainty about GDP growth due to recession fears set the table for a difficult year for stock and bond investors. Attached is a quarterly market summary; page 6 details a breakdown of the returns mapped against the most significant headlines and events from 2022.

Central Banks at home and abroad resolved to battle inflation caused market sectors, that had led the bull market since 2008, to suffer notable pullbacks. Growth sectors that benefited from an extended economic expansion and low-interest rates, such as information technology and communication services were among the worst-performing sectors in 2022. Retail stocks also tumbled as inflation drove up nondiscretionary items like food and energy, leaving less for consumers to spend on discretionary products and services. Also plaguing retailers were rising costs associated with products, services, and labor. 2022 was an especially difficult year for speculative assets like crypto, with rising interest rates and revelations of fraud and abuse impacting its viability.

Despite a difficult investment environment, a resilient consumer helped GDP rebound in the third quarter, climbing 3.2% from the prior quarter’s negative readings. Although inflation has cut into consumers’ purchasing power, consumers have continued to spend during difficult economic times, supported by rising wages, job growth, and access to savings accumulated during the pandemic.

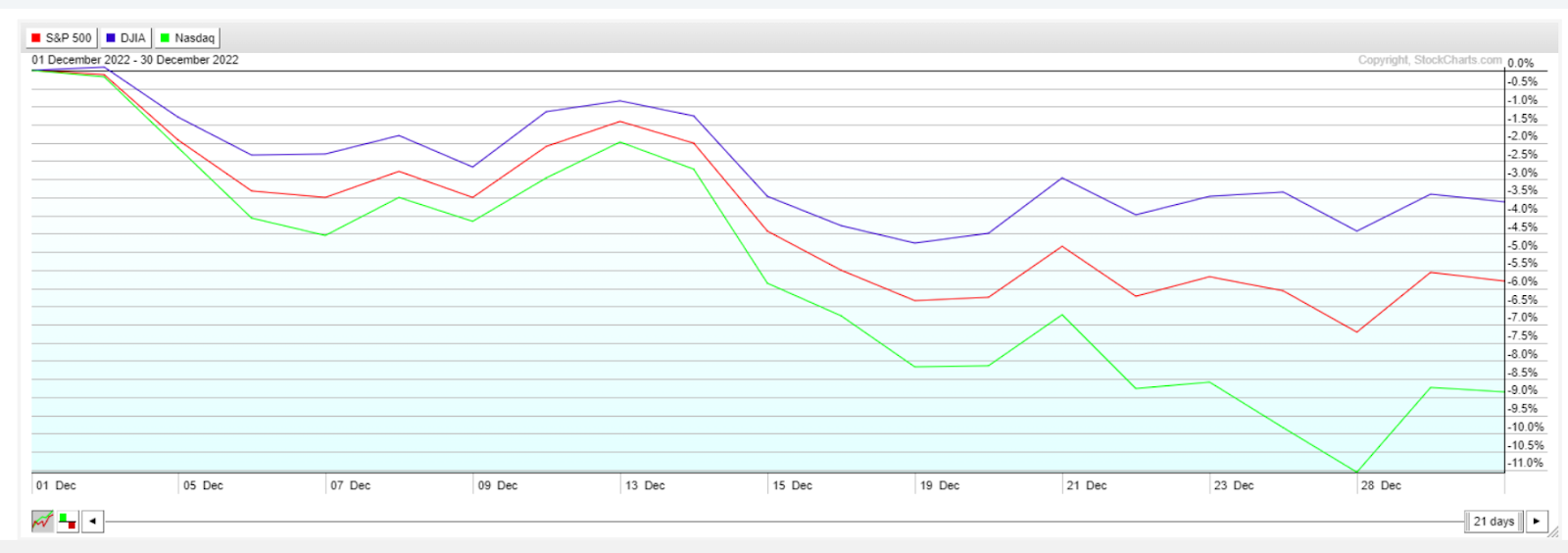

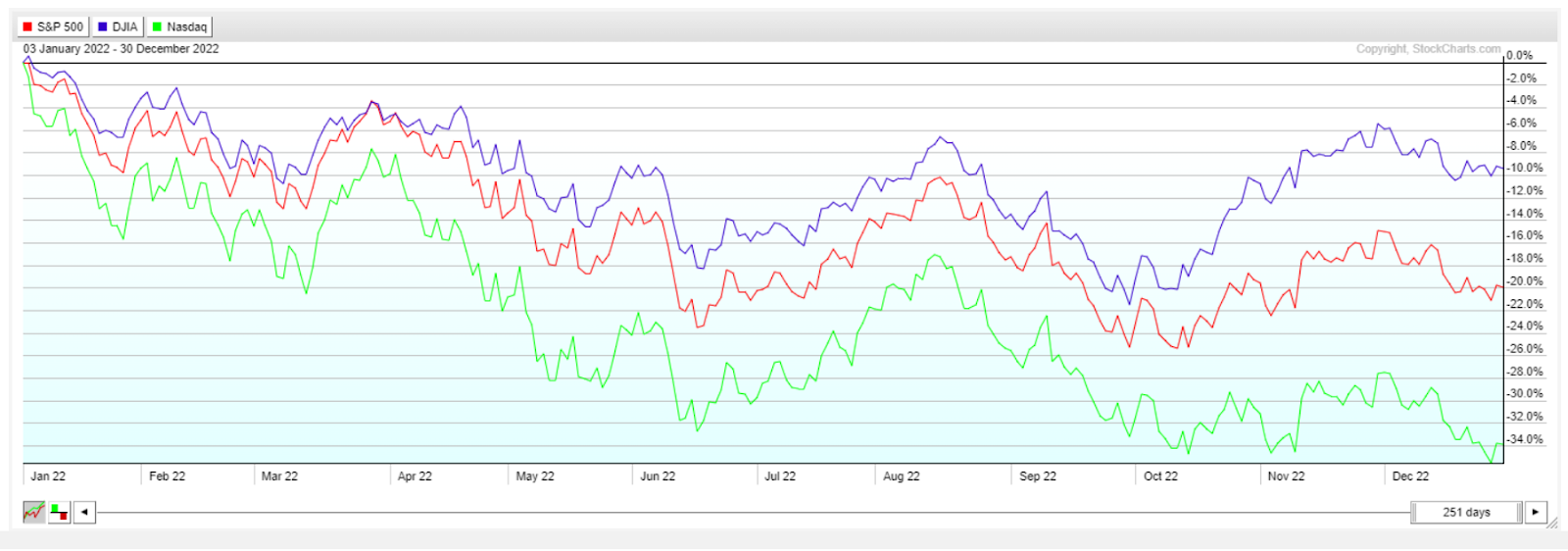

Wall Street ended December down from November and significantly down for the year. The Dow Jones Industrials (1) (blue line), S&P 500 (2) (red line), and NASDAQ (3) (green line) indexes performances diverged for the month, all posting losses in a similar fashion for which they finished the year with the Nasdaq leading the way down and the Dow Jones Industrials down, but down much less. The S&P did a bit better than splitting the difference. Higher interest rates and prospects for recession bedeviled growth stocks that rely on a growth economic environment. Growth stocks’ rich valuations coming into 2022 and the gravity of higher rates brought down the value of their long-dated expected earnings, incenting investors to rotate into stocks with high current cash flows, dividends, and lower valuations.

December 2022

Calendar Year 2022

For 2022, among the market sectors, only energy advanced, gaining a robust 59.04%. The remaining market sectors lost value, led by communication services (-40.4%) and followed by consumer discretionary (-37.6%), information technology (-28.9%), real estate (-28.5%), materials (-14.1%), financials (-12.4%), industrials (-7.1%), health care (-3.6%), consumer staples (-3.2%), and utilities (-1.4%).

We continue to believe the most likely scenario is that peak Federal Reserve hawkishness and peak inflation is behind us. That narrative continues to catch support into 2023 as consumer and producer inflation readings continue to soften, resulting in expectations for smaller rate increases and a potential rate increase pause in 2023. Whether Federal Reserve policy will deliver a soft economic landing or stall growth is the central issue markets appear to be handicapping.

Evidence of deflation exists in the decline of prices for goods as retailers put goods on sale to manage excess inventories. Also, interest-rate-sensitive sectors, such as durables and housing, have slowed dramatically due to higher interest rates. The resilient labor market has been the exception with workers being able to find jobs. The strong labor market is a two-edged sword for the Fed. Low unemployment buys time for the Fed’s rate increases, with their lagging impact, to slow the economy and bring inflation to heal. However, strong wage growth is a key measure the Fed cites as indicating there is still work to be done to curb inflation.

The Fed committee December meeting notes were released January 4th and revealed the same song, third verse; more work must be done to tame inflation. The minutes noted that Fed officials are walking the line between keeping rates high long enough to tame inflation and not being so overly restrictive for too long and slowing the economy too much, “potentially placing the largest burdens on the most vulnerable groups of the population.” This is an important point, thus far the labor market and wage growth have remained strong, However, the Bureau of Labor Statistics released their December jobs report on January 6th, 2023. The report exceeded expectations for job creation and showed slowing wage growth below expectations indicating weakening inflation pressures, the best of both worlds. Markets rallied strongly on the news enjoying its first major rally of 2023, that day Friday, January 6th. Each of the major benchmark indexes gained more than 2.0%, led by the Nasdaq (2.6%), followed by the S&P 500 (2.3%), the Russell 2000, and the Global Dow (2.2%), and the Dow (2.1%).

To summarize, economic readings are softening, and the labor markets are beginning to show signs of loosening. For the time being, with unemployment still low at 3.6% as of the December jobs report, the Fed will err on the side of tightening or at least jawboning to that effect, preferring more convincing evidence of a slowing labor market. But inflation data and now wage data appear to be trending in the right direction. The GDP expanded for the first time in the third quarter, and crude oil and gas prices reversed course and dipped lower. Primary inflationary indicators, such as the consumer price index and the personal consumption expenditures price index, trended lower at the end of the year. Ultimately, the economic outlook for 2023 will likely depend on the path of inflation, Fed policy, and whether the economies of the U.S. and the world can avoid a recession as prices are driven lower.

Looking towards 2023, we expect that if there is a recession, it will be milder than the most recent recessions because it will be an inflationary recession caused largely by Fed policy as opposed to a deflationary recession caused by a credit crisis. This scenario limits the downside for corporate earnings. Inflation readings on the decline and further loosening in the labor market will give the Fed more breathing room to refocus on its dual mandate of balancing stable prices and maintaining full employment. Despite higher rates, capital spending will grow, and financial institutions will have money to lend. In addition, the financial sector will enjoy the positive impact of higher revenues from lending at much higher margins because the rate charged for loans goes up faster than the rate paid on deposits. The technology sector will continue to be under pressure and economically sensitive stocks cyclical, which trade at relatively attractive risk premiums should benefit from improving margins. We are tilting portfolio allocations to reflect this market thesis.

Your December portfolio reports have been deposited in your eMoney vault. If you are interested in discussing our market thesis and your portfolio or in reviewing your financial plan to check your progress toward your goals, we would love to conduct a review with you. You can call us or schedule a review here.

Your December portfolio reports have been deposited in your eMoney vault. If you are interested in discussing them or any changes to your goals and objectives, we are conducting reviews and would love to discuss those with you. You can call us or schedule a review here.

Thank you for your trust and confidence!

Tim

- Dow – The Dow Jones Industrial Average (DJIA) is an unmanaged group of securities considered to be representative of the stock market in general.

- S&P 500 Index – The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

- NASDAQ – The NASDAQ) is an unmanaged group of securities considered to be representative of the stock market in general.

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation. Comments concerning the past performance are not intended to be forward-looking and should not be viewed as an indication of future results.

Converting a traditional IRA to a Roth IRA is a taxable event and could result in additional impacts to your personal tax situation, including the taxation of current social security benefit payments. Be sure to consult with a qualified tax advisor before making any decisions regarding your IRA.