Why Hike Now?: Wages

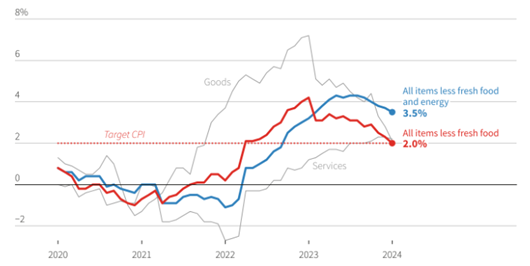

For most of the last 30 years, prices in Japan have grown at a rate below 2%. Then, like many countries around the world, Japan experienced an acceleration in inflation along with Covid-related economic policies. Beginning in 2020, Japan’s core consumer price index, less food and energy prices, began climbing and peaked at 4% in late 2022. Since then, price increases have abated and the latest reading showed 2%, in line with the BoJ’s target.

Japan’s Core Inflation Slows to Central Bank’s Target Level

Source: Reuters

So, why is the BoJ lifting rates when it has just reached its 2% target? The short answer: wage growth has not abated like prices have. As inflation picked up, Japanese workers couldn’t buy as much as they used to, much as workers in the US and elsewhere were impacted. As a result, workers in Japan have demanded higher wages and it seems they will be accommodated, with Morgan Stanley estimating average wage increases this year will be 5.2%, representing the largest pay rise in decades.

Good-Bye Carry Trade, Hello Japanese Stocks?

There are a number of implications of this change in policy. Interest rate changes encourage money to move in different directions – generally in the direction of the higher yield – and not always in intended ways. The BoJ and its negative interest rates, for instance, encouraged money to leave the country. Investors could borrow money in Japan, pay little in interest, then convert those Yen into another currency, say the US dollar, and earn a much higher level of interest here where rates are running above 5%. With Japan hiking interest rates and many other countries around the world likely to cut interest rates, this carry trade becomes much less profitable and could encourage money to move elsewhere around the globe.

This carry trade also indirectly helped the Japanese stock market. With money flowing out, the Yen weakened against other currencies. In turn, Japanese-made goods became cheaper for non-Japanese buyers, increasing exports. That higher level of exports then helped Japanese companies become more profitable. In the meantime, Japanese stocks have enjoyed their best performance in decades. After suffering through decades of economic stagnation and what became known as “the Lost Decades,” The Nikkei index recently climbed to 40,000, a level last seen in 1989. Interestingly, over the last five years, the Nikkei and the S&P 500 have had nearly identical returns.

Risks and Opportunities

In addition to ensuring continued economic growth, Japanese policymakers will have to manage two main risks: the stability of the banking system and government debt. Japan’s banks have become accustomed to ultra-low interest rates. Should rates continue to march higher, banks may struggle to manage their balance sheets much as we saw Silicon Valley Bank struggle and eventually fail last year. In addition, the government has debt that is twice the size of the economy, far higher than the US’s already high rate. With even slightly higher interest rates, the cost of servicing that debt is expected to rise substantially.

Despite the BoJ’s increase in interest rates, monetary is likely to remain accommodative. Policymakers will be watching consumer consumption patterns and capital flows to evaluate the impact of interest rate changes. In the meantime, the government is actively incenting Japanese companies to become more shareholder friendly and some well-known investors are betting that the changes will stick.

Until next time, invest wisely, and live richly,

Kara

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC do not offer tax or legal advice.