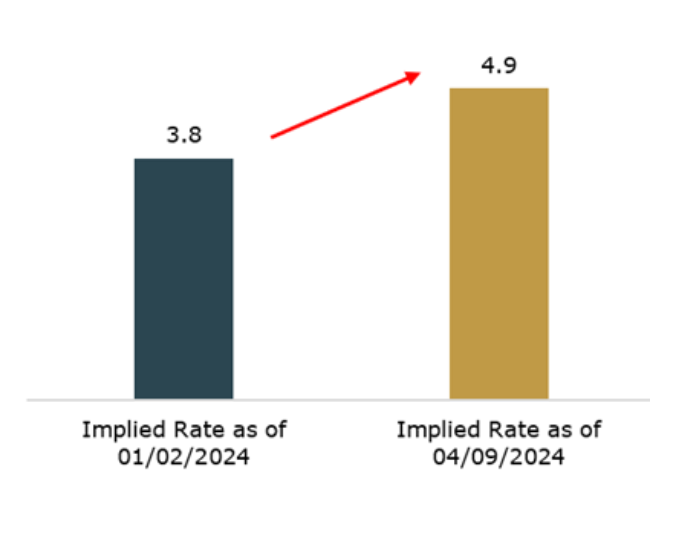

Source: Kestra Investment Management, based on Fed Funds Futures data from Bloomberg. Data as of April 15, 2024.

The Stock Market

In 2023, a handful of big tech companies (known as the Magnificent Seven) contributed the bulk of the S&P 500’s total return of more than 24%. This kind of sustained growth in a limited number of names is not unusual in the early stage of a new bull market.

Since late last year, though, this bull appears to be maturing as the broad market’s return has been driven by a larger and more-diverse group of companies in index, a trend we expect to continue. In the first quarter:

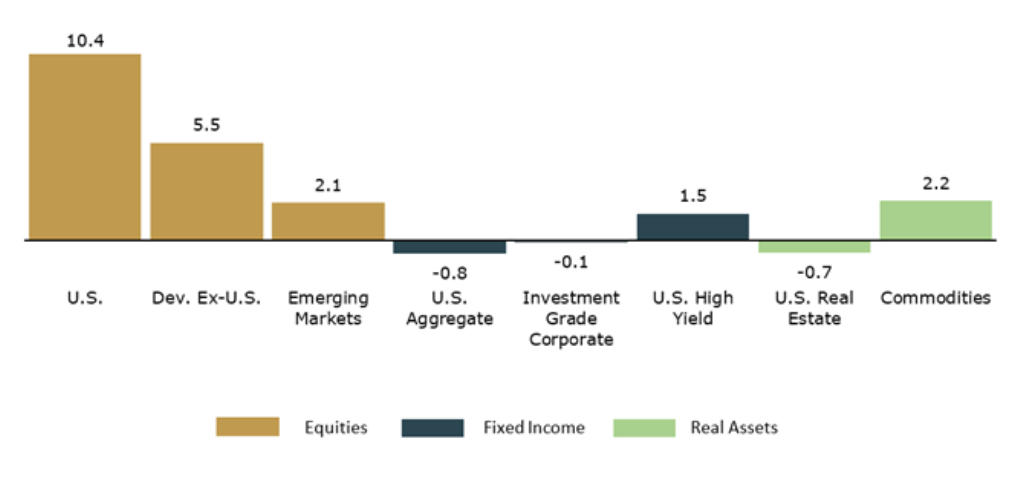

· All but one S&P 500 sector had positive returns. Only Real Estate, which is highly interest-rate sensitive, ended the quarter with negative returns.

· Higher oil prices fueled a rally in the Energy sector, which finished 2023 in the red.

· More-defensive areas of the market, such as Utilities and Consumer Staples, saw positive returns after underperforming last year.

· Mixed results among the Magnificent Seven grabbed headlines, leading Wall Street to coin a new term, Fab Four, to describe those in the group that outperformed the broader market.

Outside the concentrated, tech-heavy area of the market that drove early-stage returns, we see support for additional gains in terms of earnings and valuations. In the first quarter, the S&P 500 notched its third straight quarter of year-over-year earnings growth, according to recent estimates. For the full year, analysts expect S&P 500 earnings to grow by nearly 11% over the prior year, which, if correct, would be roughly equivalent to the index’s historical annual rate of growth for earnings.

Fixed Income

While stocks rallied in the first quarter, the returns among bonds were less impressive. Overall performance was slightly negative to flat, with the exception of high yield bonds, which increased nearly 2%.

Given today’s high yields, we continue to see opportunity in the bond market, with some caveats. If the Fed cuts rates this year, shorter-term yields are likely to decline, potentially reducing future returns for investors with heavy exposure to cash equivalents. What’s more, the recent surge in Treasury issuance may create volatility among longer-term bonds. In our view, the so-called belly (or middle) of the yield curve is better insulated from both these risks.

It’s also worth noting that we prefer high grade corporate bonds to high yield given the uptick in corporate bankruptcies, which hit a three-year high in 2023.

The Takeaway

The U.S. economy has shown remarkable resilience, and we expect it to continue to grow this year. That said, the inflation picture, the presidential election and geopolitical risks (namely the wars in Ukraine and Gaza) may contribute to the kind of market volatility we saw in earlier this month.

When it comes to the election, the good news is that its effect on the market is likely to be short-lived. Our analysis of long-range historical data shows that volatility tends to be higher during election years, but most of the time, the market ends the year on a high note.

The balance of this year may look a lot like the often-fitful transition from spring to summer – one day the sun shines, the next cold rain, followed by more sun. In fact, the Fed has warned that the path back to its target inflation rate of 2% may be bumpy. As always, a well-diversified portfolio can help investors ride out the inevitable dark days and stay focused on their long-term goals.

Invest wisely and live richly,

Kara